Saudi Arabia’s real estate market is no longer defined by ambition alone. In 2026, it is defined by execution, capital flow, and measurable pressure on supply.

Over the past few years, the Kingdom has moved from policy announcements to physical delivery. Residential launches in Riyadh have accelerated. Mega-projects are transitioning from concept to construction phases. Mortgage penetration continues to expand among Saudi nationals, while regulatory shifts are gradually opening segments of the market to foreign buyers and institutional investors. What used to be speculative momentum has turned into structured growth.

At the same time, the market is entering a more complex phase. Housing prices in northern Riyadh are rising faster than income growth. Rental demand in Jeddah is tightening in selected districts. The Eastern Province continues to show stable but slower absorption rates compared to the capital. Developers face a new reality: scale is no longer enough — operational discipline, liquidity planning, and demand forecasting matter more than launch volume.

This is what makes 2026 a critical year for the Saudi Arabia real estate market.

In this analysis, we break down:

-

the macroeconomic forces shaping property demand,

-

residential price movements across major cities,

-

investment flows and yield expectations,

-

the real impact of Vision 2030 on housing development,

-

and the structural risks that could define the next phase of the cycle.

Whether you are an investor evaluating returns, a developer planning supply, or an institutional player monitoring capital allocation, understanding the dynamics behind the headlines is essential. Saudi Arabia’s property market is expanding — but it is also maturing. And maturity changes the rules of growth.

Table of Contents

Executive Overview: The Market Has Shifted from Growth to Structure

Saudi Arabia’s real estate market in 2026 is often framed as a success story of Vision 2030. And while growth is real — in transactions, project launches, and foreign interest — the deeper shift is structural.

The Kingdom is no longer simply stimulating housing demand. It is redesigning urban density, mortgage accessibility, capital participation, and investor governance simultaneously. What makes 2026 different is not speed. It is maturity. Markets that once expanded on macro stimulus alone are now evaluated on pricing discipline, absorption logic, infrastructure alignment, and execution consistency.

Growth is no longer the headline. Sustainability is.

Macro Foundations: Vision 2030 and Structural Reform

To understand Saudi Arabia’s property trajectory, you have to start with Vision 2030 — not as a slogan, but as a capital allocation strategy.

The Kingdom’s economic diversification plan has moved substantial public and sovereign capital into infrastructure, tourism, logistics, entertainment, and urban redevelopment. Riyadh’s transformation into a regional business hub, giga-projects like NEOM and the Red Sea development, and large-scale public investments in transport and public space have all created real, not speculative, real estate multipliers.

But diversification also changed household economics. Non-oil sector employment is expanding. Female labor force participation has increased materially over the past several years. Mortgage penetration has improved compared to pre-2016 levels. These are not cosmetic statistics; they translate into household formation, purchasing power, and urban migration patterns.

Importantly, housing is a policy metric. The government’s homeownership target — set at 70% by 2030 — is not symbolic. It drives financing programs, developer incentives, and supply acceleration. This alignment between policy and housing demand reduces the probability of abrupt contraction, even if segments fluctuate.

Demand Engines: Who Is Driving the Market

The Saudi real estate market in 2026 is powered by three overlapping demand blocks.

Domestic Household Formation

Saudi Arabia’s demographic profile supports housing absorption structurally. A young median age means household formation will continue expanding into the late 2020s. Riyadh benefits disproportionately due to employment centralization and public-sector relocations.

Buyer behavior is also shifting. Traditional preference for standalone villas is gradually giving way to townhouses and mid-density community housing where land economics allow pricing discipline without sacrificing lifestyle.

Urban Migration

Riyadh’s status as a regional headquarters hub has direct housing consequences. Domestic migration into the capital increases pressure on both purchase and rental markets. This pressure has already triggered regulatory attention regarding rental inflation.

Foreign Buyers and Cross-Border Capital

The extension of foreign ownership rights in designated zones is not yet creating speculative surges, but it has changed buyer composition. Remote purchasing, cross-border documentation, and investor-driven acquisitions are more common in 2026 than five years earlier.

The result is a more complex transaction environment. Developers face not just volume growth, but process complexity growth.

Supply Landscape: Ambition Meets Absorption Reality

On paper, supply pipelines appear robust across residential, mixed-use, and hospitality segments. But supply type matters more than supply volume.

The current market can be segmented into four structural residential categories:

| Segment | Core Buyer | Pricing Sensitivity | Absorption Pattern | Systemic Risk |

|---|---|---|---|---|

| Affordable/Mid-Market Apartments | Mortgage-backed families | High | Steady | Lower |

| Townhouses / Mid-Density Communities | Upgrading households | Medium | Balanced | Moderate |

| Luxury Villas | High-net-worth | Low | Cyclical | Higher |

| Branded Mixed-Use / Giga-Projects | Investors + HNWIs | Low | Phased | Capital-dependent |

While high-profile developments capture international headlines, the majority of real absorption remains anchored in mid-market segments.

The strategic tension lies here: prestige projects elevate the national brand, but mid-density housing stabilizes transaction velocity.

Pricing Evolution 2020–2026

Price behavior across Saudi Arabia’s main urban hubs illustrates structural divergence.

Residential Price Index Movement (Illustrative Trend Model)

| City | 2020 (Index = 100) | 2022 | 2024 | 2026 Est. | Structural Driver |

|---|---|---|---|---|---|

| Riyadh | 100 | 112 | 128 | 140–150 | HQ relocation + infrastructure |

| Jeddah | 100 | 108 | 118 | 125–130 | Trade + tourism expansion |

| Eastern Province | 100 | 104 | 112 | 118–122 | Energy sector stability |

Riyadh’s divergence reflects concentrated capital injection and migration. However, elevated growth invites regulatory sensitivity, especially where affordability tensions emerge.

Price acceleration without income growth eventually triggers political and financial balancing measures. Saudi Arabia’s regulatory apparatus has shown willingness to intervene when rental or housing inflation accelerates too quickly.

Price Comparison: Townhouses, Villas, Penthouses and Luxury Homes (2026 Snapshot)

Saudi Arabia’s residential market has become increasingly tiered. Price segmentation between mid-market and luxury assets has widened, particularly in Riyadh and Jeddah.

Below is an indicative comparison based on 2026 market positioning:

| Property Type | Riyadh (SAR) | Jeddah (SAR) | Eastern Province (SAR) | Typical Buyer Profile |

|---|---|---|---|---|

| Townhouses | 1.1M – 2.2M | 1.0M – 2.5M | 900K – 1.8M | Young families, first-time buyers |

| Standalone Villas | 1.8M – 4.5M | 2.0M – 5.0M | 1.5M – 3.5M | Established households |

| Penthouses | 3.5M – 8M+ | 4M – 9M+ | 3M – 6M | High-income professionals |

| Ultra-Luxury Estates | 10M+ | 12M+ | 8M+ | HNWIs, institutional buyers |

What This Tells Us

Townhouses remain the liquidity engine of the residential market. They offer the strongest absorption rates due to relative affordability and mortgage accessibility.

Standalone villas are stable but increasingly sensitive to pricing pressure in oversupplied districts.

Penthouses and waterfront luxury apartments are benefitting from international attention, particularly in Jeddah’s northern coastal zones and select Riyadh vertical developments.

Ultra-luxury estates represent a thin but high-value segment, often linked to strategic zones or branded residences.

The widening price gap reflects economic diversification. A stronger professional class supports high-end demand, while mortgage expansion sustains mid-market housing.

Rental Market: Yield, Stability, and Segment Divergence

Rental economics remain attractive relative to many global markets, but yield distribution varies by segment.

Typical gross residential yields in 2026:

-

Mid-density communities: 5–7%

-

Standard apartments in stable zones: 4–6%

-

Luxury villas: 3–5%

Riyadh’s rental demand remains structurally supported by inbound labor mobility. Yet rent pressure has reached a level where regulatory oversight has increased visibility.

Yield stability favors disciplined community-based developments over isolated luxury inventory.

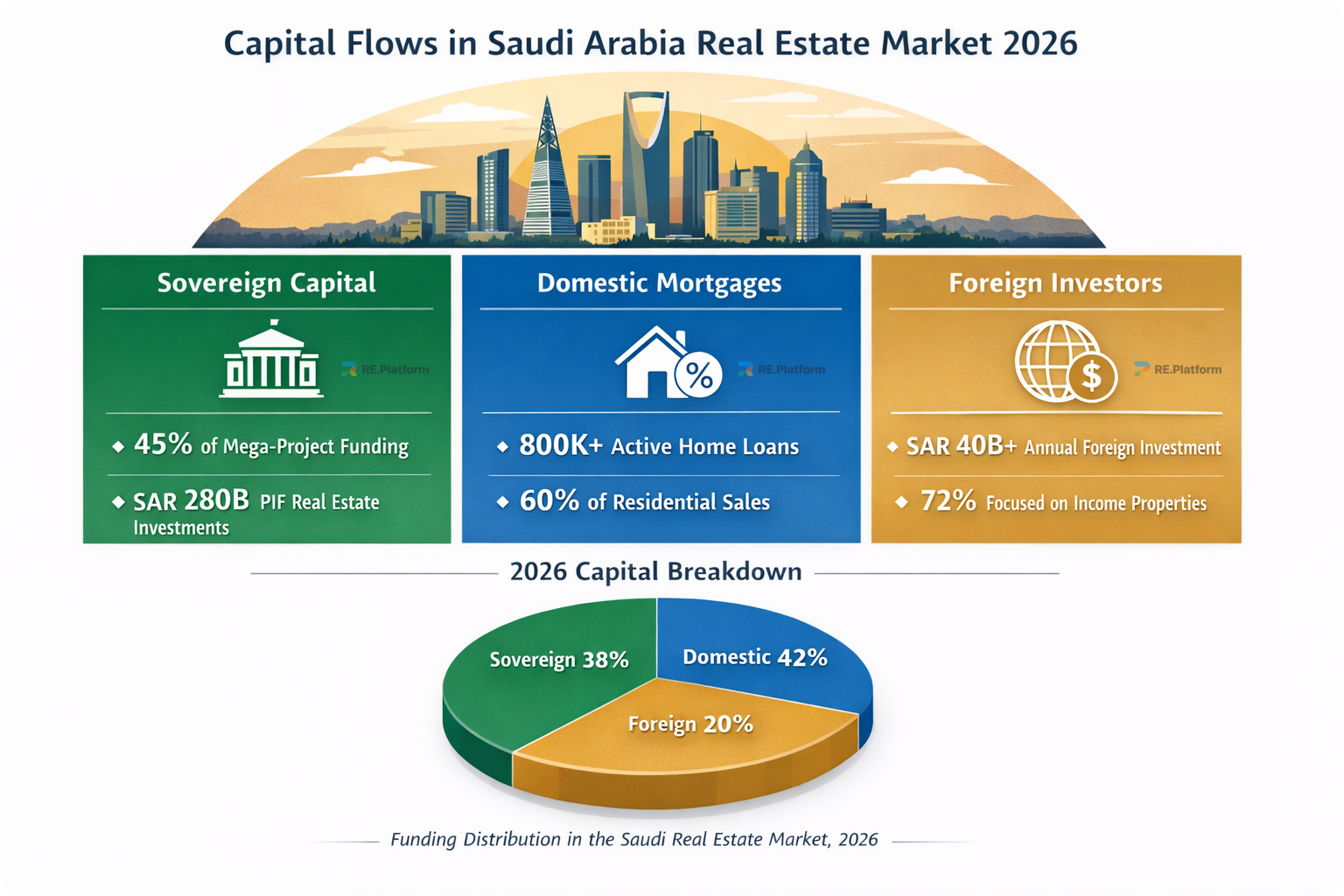

Capital Flows: Where the Money Is Actually Moving

Behind the headlines about mega-projects and giga-developments lies a more nuanced capital structure. The Saudi real estate market in 2026 is not fueled by speculative retail buying — it is driven by three distinct sources of capital: sovereign-backed investment, domestic mortgage expansion, and selectively returning foreign interest.

Public Investment Fund (PIF) remains the gravitational center. Through direct development vehicles and strategic stakes in master developers, sovereign capital continues to anchor large-scale urban expansion — particularly in Riyadh and the Red Sea corridor. However, 2025–2026 marks a subtle shift: projects are expected to demonstrate absorption discipline, not just architectural ambition. Capital is becoming more performance-sensitive.

On the domestic front, mortgage penetration has expanded significantly compared to pre-Vision 2030 levels. Saudi banks report sustained housing finance growth, particularly among first-time buyers. Residential lending volumes remain structurally higher than five years ago, even as interest rate conditions fluctuate. The result is stable end-user demand in mid-market housing rather than speculative flips.

Foreign capital is returning more selectively. International private equity and family offices are increasingly targeting:

-

income-generating residential compounds,

-

mixed-use developments in Riyadh,

-

logistics-linked real estate in the Eastern Province.

However, the market has not yet reached the scale of institutional foreign inflows seen in mature markets. Investors are watching execution risk, delivery timelines, and regulatory clarity.

The conclusion is clear: Saudi real estate in 2026 is capital-backed, but capital is no longer blindly expansionary. It is moving toward disciplined growth.

The Developers Shaping Saudi Arabia’s Housing Landscape

No analysis of the Saudi property market is complete without examining the developers executing Vision 2030 at scale. While capital sets direction, developers determine delivery quality, pricing dynamics, and market credibility.

Several names dominate current residential transformation for real estate development:

-

ROSHN Group – backed by PIF, ROSHN has become one of the largest master residential developers in the Kingdom, focusing on integrated communities designed for Saudi families.

-

Emaar The Economic City – instrumental in King Abdullah Economic City, reshaping mixed-use coastal urban models.

-

Dar Al Arkan – a long-standing private developer active in luxury residential and international expansion.

-

Jabal Omar Development Company – central to high-value projects in Makkah.

-

Retal Urban Development – increasingly visible in mid-scale and mixed housing developments.

These firms operate at different price segments — from mass housing to ultra-luxury — but collectively define supply pipeline credibility.

By the way, if you’re a developer in Saudi Arabia, be sure to read our article about CRM for Real Estate developers. It’s helpful.

The competitive landscape among developers is evolving. Speed of launch is no longer the only metric of success. Buyers and investors now examine:

-

delivery history,

-

infrastructure readiness,

-

community integration,

-

and long-term value preservation.

Brand trust is becoming a pricing premium factor.

A Market Moving Toward Institutional Discipline

Saudi Arabia’s real estate market in 2026 is structurally strong, policy-aligned, and capital-backed. Demographics support housing demand. Infrastructure spending reinforces urban concentration. Regulatory frameworks are more mature than a decade ago.

But the era of opportunistic, loosely structured expansion is closing.

The winners of the next phase will not simply be those who launch the largest projects. They will be those who align pricing, supply pacing, operational rigor, and buyer transparency into a unified system.

Saudi Arabia is not just expanding its skyline. It is building a real estate ecosystem that increasingly resembles institutional markets.

The question is no longer whether growth exists. It is whether that growth can be executed precisely.

FAQ

Is the Saudi Arabia real estate market still growing in 2026?

Yes. Structural demand, infrastructure investment, and policy-backed housing initiatives continue to support expansion, particularly in Riyadh.

Which city offers the strongest investment case?

Riyadh currently demonstrates the strongest structural growth due to employment concentration and infrastructure investment, though Jeddah and selected Eastern Province zones remain attractive.

Are foreign investors actively participating?

Participation is increasing in designated zones, though flows are selective and governance-sensitive rather than speculative.

What is the primary risk in 2026?

Operational and pricing imbalance rather than systemic collapse. Overextension in luxury segments and execution gaps represent more realistic concerns.

Other Articles:

Why Investors Misjudge the Saudi Arabia Real Estate Market

Is Rental Income Taxed in Saudi Arabia? A Complete 2026 Guide for Property Investors

Property for Sale in Jeddah: Prices, Districts, and How to Find Real Projects in 2026

Property for Sale in Riyadh: Where to Buy, Prices in 2026, and How to Find Real Projects

How to Search Apartments for Sale in Saudi Arabia: A Smarter Approach in 2026

$3.4B of Demand, Limited Access: The Real Story Behind Branded Residences in Saudi Arabia

Why You Still Can’t Freely Buy Property in Saudi Arabia in 2026